Summary: On-chain KYC is an identity verification mechanism based on blockchain, verifiable credentials, and cryptographic proofs. It allows Web3 applications to verify whether a user has completed KYC or meets specific conditions such as jurisdiction, age, or investor eligibility, while avoiding the direct exposure of raw identity information such as ID documents, passports, or facial data on-chain. This article explains the core value, technical architecture, and application scenarios of on-chain KYC, and how it can help Web3 identity verification balance compliance, privacy, and decentralization.

Introduction: Why Web3 Needs On-chain KYC and a New Identity Layer Now

Over the past few years, the core narrative of Web3 has been openness, permissionless access, and user ownership of assets. Self-custodial wallets, peer-to-peer transfers, DeFi, and on-chain transactions have all developed around this logic.

However, as Web3 moves into stablecoin payments, RWA, PayFi, lending, merchant services, and on-chain financial products, a wallet address alone is no longer enough. Real-world finance does not only care whether an address can initiate a transaction. It also needs to determine whether a user is eligible to participate, whether a merchant has completed KYB, whether a jurisdiction is allowed, and whether an investor meets the access requirements for a specific product.

This is why on-chain KYC has become increasingly important at this stage.

Four Real-world Drivers Behind On-chain KYC

- Regulatory pressure: The FATF Travel Rule requires virtual asset service providers to obtain and retain relevant information about the originator and beneficiary in virtual asset transfers. The EU’s MiCA framework has also brought stablecoins, CASPs, ARTs, and EMTs into a clearer regulatory structure. Stablecoins and crypto services are moving from early-stage experimentation toward more regulated and licensed operations.

- Business demand: Scenarios such as RWA, stablecoin payments, lending, merchant settlement, and compliant DeFi cannot rely on a wallet address alone to determine user eligibility. For example, RWA products need to assess investor eligibility, jurisdictional restrictions, and transfer rules. Stablecoin payment applications may need tiered limits, merchant KYB, and jurisdictional access controls. Lending products may require risk levels or credit conditions.

- Historical issues: Many on-chain projects have faced problems because of fully anonymous and open participation, including Sybil attacks, airdrop farming, restricted-region access, illicit fund flows, and a lack of effective access control. KYC is not designed to solve every security issue, but it can help answer one specific question: who is eligible to use a certain product or service?

- Product evolution: Web3 is moving from “just trading” toward real-world financial services. Once an application involves stablecoin payments, RWA, PayFi, compliant yield products, or merchant services, it needs an identity layer that is better suited to on-chain environments than traditional KYC.

Therefore, what Web3 needs is not to simply move traditional KYC onto the blockchain, nor to publicly upload users’ ID documents, passports, addresses, or facial data to a public chain. A more reasonable direction is to build a new on-chain identity verification mechanism: users complete identity verification off-chain, hold their own identity credentials, and prove to different applications when needed that they meet certain conditions.

The value of on-chain KYC is not to guarantee that a user will always be trustworthy. Instead, it provides DeFi, stablecoin payments, RWA, and on-chain financial applications with a verifiable, reusable, and privacy-preserving compliance signal.

What Is On-chain KYC?

On-chain KYC refers to an identity verification framework that uses blockchain and cryptographic mechanisms to allow applications to verify whether a user meets specific identity or compliance conditions. Many people mistakenly assume that on-chain KYC means writing personal information such as ID documents, passports, addresses, or facial data directly onto a public blockchain. In reality, a properly designed, privacy-focused on-chain KYC system should not work this way.

A more appropriate model is:

- The user first completes off-chain identity verification with a trusted identity issuer or KYC service provider.

- The issuer verifies the user’s information off-chain.

- Once verification is passed, the issuer signs and issues an encrypted identity credential to the user.

- The user stores this credential in a wallet or local identity environment.

- When a DApp needs to verify an identity condition, the user generates a proof based on the credential.

- An on-chain verification contract or verifier checks the proof and returns a pass or fail result.

In this process, the DApp does not need to see the user’s full identity profile, the blockchain does not need to store raw personal information, and the user does not need to repeatedly submit KYC materials to every application.

This is the core value of on-chain KYC: it can serve as a reusable compliance identity layer for Web3.

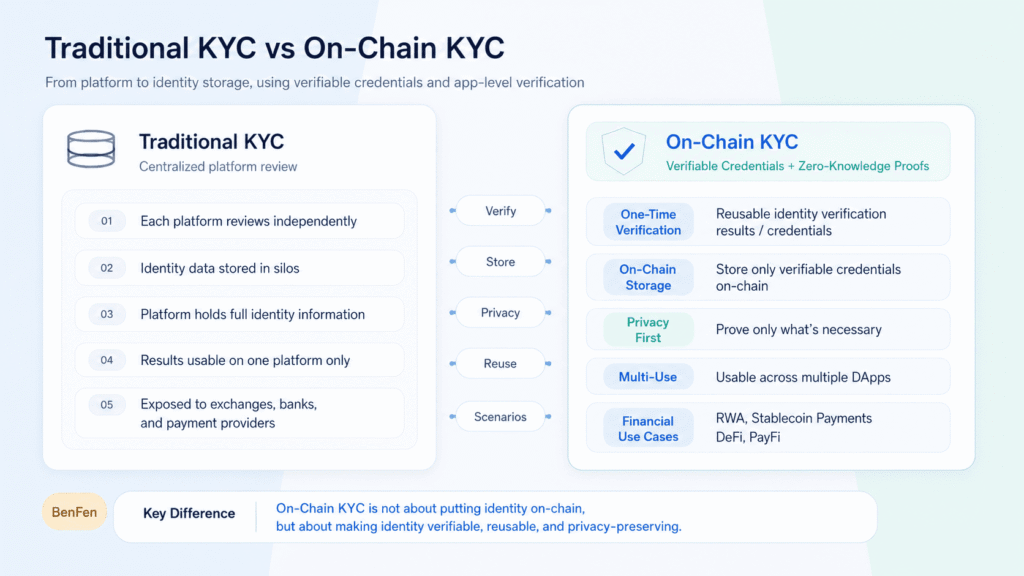

How Is On-chain KYC Different from Traditional KYC?

The core difference between traditional KYC and on-chain KYC is not only the verification process. It also lies in how identity data is stored, how verification results can be reused, and how privacy can be protected.

| Comparison Dimension | Traditional KYC | On-chain KYC |

| Verification Method | Each platform verifies the user’s identity separately | Users complete verification once and reuse the result through credentials or proofs |

| Data Storage | Identity data is usually stored centrally by the platform | Raw identity data remains off-chain, while credentials or proofs are verified on-chain |

| Privacy Protection | Platforms usually hold relatively complete user identity information | Selective disclosure and zero-knowledge proofs can be used to verify only necessary conditions |

| Reusability | Verification results are usually limited to a single platform | Identity credentials can be used across multiple DApps or on-chain applications |

| Application Scenarios | Centralized platforms such as exchanges, banks, and payment companies | RWA, stablecoin payments, DeFi, PayFi, and on-chain financial applications |

Traditional KYC is usually platform-centered. Each exchange, payment company, financial application, or service platform requires users to submit identity materials separately. After completing the review, the platform stores the user’s information in its own database and decides whether the user can access certain services. This model has several clear limitations.

- First, users need to repeatedly submit the same materials across multiple platforms, making the registration and onboarding process cumbersome.

- Second, platforms become centralized storage points for sensitive personal data. If a database is compromised, users may face identity theft, phishing attacks, and asset security risks.

- Third, identity verification results are difficult to reuse. Even if a user has completed verification on one platform, it is hard to bring that result to another application.

- Fourth, compliance decisions are usually hidden inside centralized systems. Users and developers often have limited visibility into how access permissions are granted or rejected.

On-chain KYC changes this structure. It does not require every application to collect and store complete identity data. Instead, it uses cryptographic proofs to verify specific identity conditions. For example, a DApp may only need to know that:

- the user has completed KYC;

- the user is over 18 years old;

- the user is not from a restricted jurisdiction;

- the user is eligible to participate in a specific investment product;

- the user has passed a certain risk-level review.

In these scenarios, the DApp does not necessarily need to know the user’s name, address, ID number, or complete identity record. This makes on-chain KYC more suitable for Web3 environments that require privacy protection and composable applications.

The Core Value of On-chain KYC

The value of on-chain KYC is not simply about moving identity verification results onto the blockchain. More importantly, it provides Web3 applications with a new way to coordinate identity: users do not need to repeatedly submit complete identity documents to every application, and applications do not need to directly store large amounts of sensitive personal data. Instead, applications can use verifiable credentials and on-chain verification logic to determine whether a user meets a specific condition.

- Reducing Repeated KYC Costs

Under the traditional KYC model, users often need to resubmit ID documents, passports, proof of address, facial verification, and other materials every time they join a new exchange, payment platform, financial application, or service provider. Even if a user has already completed verification on another platform, that result is usually difficult to reuse.

On-chain KYC can improve this process. After completing off-chain identity verification once, users can hold an identity credential issued by a trusted issuer. When different DApps or on-chain financial applications need to verify a user’s identity conditions, the user can generate proofs based on the same credential instead of repeatedly submitting full KYC materials.

This can lower the entry barrier for users accessing Web3 financial applications, while also reducing repetitive costs for applications in identity review, data collection, and user support.

- Reducing the Need for Applications to Store Sensitive Identity Data

Another issue with traditional KYC is that platforms often become centralized storage points for sensitive personal data. Users’ ID documents, addresses, facial verification data, and other personal information may be stored separately across multiple platforms. If one of these databases is compromised, users may face identity theft, phishing attacks, and asset security risks.

On-chain KYC does not require applications to directly store users’ complete identity information. A more reasonable model is to keep raw identity data off-chain, while a trusted issuer completes the verification and issues a credential. The application only needs to verify whether the user meets a certain condition, such as whether they have completed KYC, meet an age requirement, come from an allowed jurisdiction, or are eligible to participate in a specific product.

This reduces the scope of sensitive data that applications directly handle and makes identity verification closer to “proof on demand” rather than excessive data collection.

- Making Compliance Rules Programmable

In traditional financial systems, many compliance decisions take place in centralized back-end systems. They are difficult for external applications to reuse and difficult to integrate directly with smart contracts. For Web3 applications, if identity conditions cannot be recognized by smart contracts, many financial rules can only rely on manual review, centralized whitelists, or off-chain systems.

The value of on-chain KYC is that it can turn certain identity conditions into verifiable and programmable rules. For example, an RWA product may require users to prove that they have completed KYC and are not from a restricted jurisdiction before they can subscribe. A stablecoin payment application may verify a user’s identity status before enabling higher limits. A lending product may decide whether a user can access a specific market based on whether they meet certain conditions.

This does not mean that all compliance processes can be fully automated, nor does it mean that on-chain KYC can replace legal, custody, or regulatory requirements. But it can make it easier for on-chain applications to execute access rules, limit rules, jurisdictional rules, and eligibility checks at the protocol level.

- Providing a Reusable Identity Foundation for Stablecoins, RWA, PayFi, and On-chain Financial Products

As Web3 moves from on-chain trading toward real-world financial services, the identity layer becomes increasingly important. Stablecoin payments need to handle limits, merchants, jurisdictions, and risk tiers. RWA products need to manage investor eligibility, transfer restrictions, and redemption rules. PayFi applications need to connect on-chain assets with real-world payment scenarios. Lending, compliant yield products, and institutional financial products also require clearer access mechanisms.

If every application builds its own identity system from scratch, it will not only be inefficient but also create fragmented data and repetitive user experiences. On-chain KYC can serve as a reusable identity infrastructure layer, allowing different applications to call trusted identity credentials and verification results without repeatedly collecting complete identity materials.

Therefore, the core value of on-chain KYC is not to make Web3 more closed. Instead, it is to give scenarios that require compliant access a safer, more privacy-friendly, and more composable identity verification method. It provides a foundation for connecting real-world rules with on-chain application logic across stablecoins, RWA, PayFi, and on-chain financial products.

The Core Architecture of On-chain KYC

A complete on-chain KYC system should not simply move a Web2-style centralized identity database onto the blockchain. Its core goal is to make identity verification results recognizable and usable by on-chain applications, while preventing raw identity data from being publicly exposed.

Therefore, on-chain KYC is usually not a single function. It is an identity verification process composed of users, issuers, identity credentials, verifiers, verification requesters, zero-knowledge proofs, and credential management mechanisms.

- User: Completing Verification and Self-holding Credentials

The user is the starting point of the identity verification process. First, the user completes off-chain identity verification with a trusted identity issuer or KYC service provider, such as by submitting ID documents, passports, proof of address, facial verification, or corporate information.

After verification is passed, the user should not need to resubmit complete identity materials every time they use a new application. A more reasonable approach is for the user to hold an identity credential issued by the issuer and authorize the use of that credential when needed, proving to different applications that they meet specific identity conditions.

In this model, the user is not only a passive subject of platform review, but also the holder and authorizer of their own identity credential.

- Issuer: Completing Off-chain KYC and Issuing Identity Credentials

The issuer is responsible for executing or confirming off-chain KYC. It may be a regulated KYC service provider, an identity verification institution, a compliance partner, or an authorized identity issuer within an ecosystem.

The issuer’s role is not simply to give the user a “passed” label, but to sign and confirm certain verified identity facts.

For example:

- KYC has been completed;

- age requirements are met;

- jurisdictional access conditions are satisfied;

- qualified investor status is confirmed;

- a corporate entity has completed KYB;

- a specific risk level or compliance condition is met.

These signed identity facts can become identity credentials that the user later uses in Web3 applications.

- Identity Credential: Carrying Verifiable Identity Conditions

An identity credential is a cryptographic statement signed by an issuer. It does not need to contain complete raw identity data. Instead, it can represent certain verified facts or attributes.

For example, an identity credential may prove that a user has completed KYC, or that the user meets certain requirements related to jurisdiction, age, risk level, or investment eligibility. What the application needs to verify is whether “this condition is true,” not necessarily the user’s name, address, ID number, or complete identity profile.

The key value of an identity credential is verifiability. Applications can check whether it was issued by a trusted issuer, whether it has been tampered with, whether it is still valid, and whether it satisfies current business rules.

- Verifier: Checking Proofs and Returning Verification Results

The verifier is responsible for checking whether the proof submitted by the user satisfies the required rules. In Web3 scenarios, the verifier may be an on-chain verification contract or a verification module that works together with on-chain logic.

The verifier does not need to receive the user’s complete identity materials. It only needs to determine whether the proof submitted by the user is valid and whether it satisfies the identity conditions defined by the application.

The verification result can be very simple: pass or fail.

For example, an RWA platform may only need to know whether the user is eligible to subscribe. A stablecoin payment application may only need to know whether the user has completed the required level of identity verification. A lending product may only need to know whether the user satisfies a specific risk or access condition.

- Verification Requester: Defining Specific Identity Conditions

The verification requester is the application, protocol, or service that needs identity verification. It may be an RWA issuance platform, a stablecoin payment application, a lending protocol, a merchant service platform, a DAO governance system, a token issuance platform, a cross-border payment application, or an on-chain financial product.

The verification requester defines the specific identity condition. The user then generates a proof based on their credential, and the verifier checks the result.

- Zero-knowledge Proofs: Reducing Unnecessary Identity Exposure

Zero-knowledge proofs are an important privacy-preserving mechanism in on-chain KYC. They allow users to prove that they satisfy a certain condition without revealing the underlying identity data.

For example, a user can prove that they are over 18 without disclosing their exact date of birth. They can prove that they have completed KYC without revealing their ID number or passport information. They can prove that they are not from a restricted jurisdiction without disclosing their full address.

This shifts on-chain KYC away from “giving more identity information to applications” and toward “proving only what the current scenario requires.”

- Credential Revocation and Expiry: Keeping Identity Status Up to Date

On-chain KYC also needs to support credential revocation and expiry mechanisms, because a user’s identity status is not permanent.

For example, compliance rules in a user’s jurisdiction may change; some credentials may expire; user eligibility may need to be reassessed; a corporate KYB status may need to be updated; or a credential issued by a certain issuer may be revoked due to risk reasons.

Without revocation and expiry mechanisms, on-chain KYC can easily become a one-time verification model and fail to meet the dynamic compliance requirements of real-world financial scenarios.

Therefore, a complete on-chain KYC architecture usually needs to support credential validity periods, revocation lists, status updates, and re-verification mechanisms.

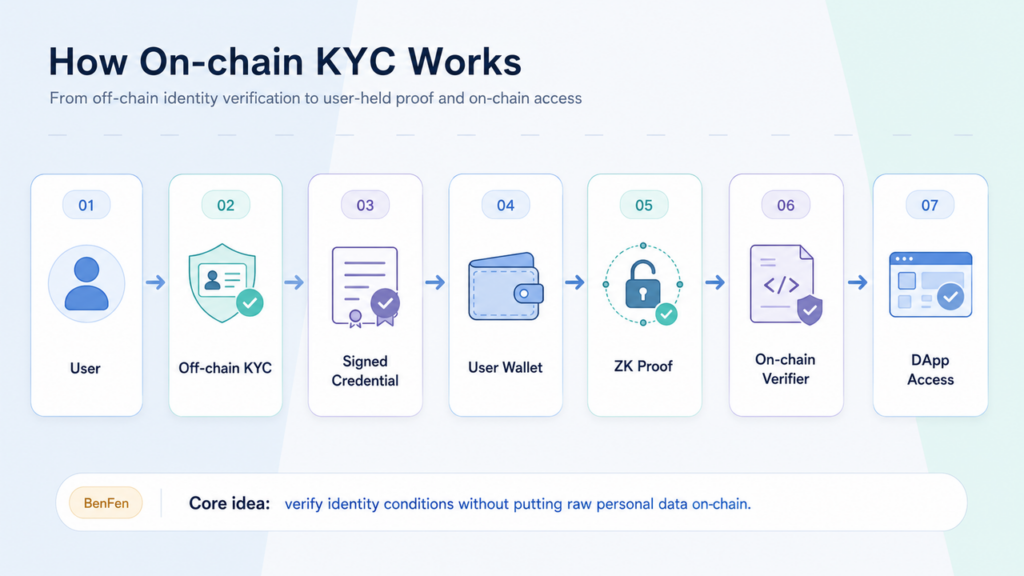

- A Complete On-chain KYC Flow

In summary, a typical on-chain KYC flow can be described as follows:

- The user completes KYC or KYB off-chain;

- The issuer verifies the user’s information;

- The issuer signs and issues an identity credential to the user;

- The user self-holds the credential;

- A DApp defines a specific identity verification condition;

- The user generates a proof based on the credential;

- A verifier or on-chain verification contract checks the proof;

- The application receives a pass or fail verification result;

- The credential supports expiry, updates, or revocation based on predefined rules.

This architecture allows identity verification to become part of Web3 infrastructure, instead of turning public blockchains into public identity databases.

A well-designed on-chain KYC architecture should follow four principles: privacy, portability, programmability, and compliance flexibility. It should enable applications to verify necessary identity conditions while minimizing the exposure of sensitive user information. It should support real-world financial scenarios such as RWA, stablecoin payments, PayFi, lending, and merchant services, while avoiding repeated collection and storage of complete user identity data by every application.

Typical Application Scenarios for On-chain KYC

On-chain KYC can support multiple Web3 use cases.

- RWA Issuance and Trading

RWA tokenization often involves investor eligibility, jurisdictional restrictions, subscription conditions, holding rules, transfer restrictions, income distribution, and redemption processes. A wallet address alone is not enough to determine whether a user is eligible to participate in a certain asset.

On-chain KYC can help RWA platforms verify whether a user has completed KYC, comes from an allowed jurisdiction, and meets investor eligibility requirements before subscription, holding, transfer, or redemption. It cannot replace legal documents, custody arrangements, or regulatory processes, but it can make on-chain access rules for RWA more programmable and verifiable.

- Stablecoin Payments and PayFi

When stablecoin payment and PayFi applications enter real-world payment scenarios, they often need to handle tiered limits, merchant KYB, jurisdictional access, payment eligibility, and risk management.

On-chain KYC allows users or merchants to prove that they meet certain identity conditions without repeatedly submitting complete identity materials. For example, a user may prove that they have completed KYC before enabling higher payment limits, while a merchant may prove that it has completed KYB before opening collection and settlement services. This can help balance compliance, privacy, and user experience.

- DeFi Lending and Institutional Financial Products

Open DeFi does not necessarily require KYC. However, institutional pools, credit-based lending, undercollateralized lending, permissioned lending markets, and compliant yield products often require more identity and risk information.

On-chain KYC can help protocols determine whether a user has completed KYC, whether the user is an institutional participant, whether the user meets a certain risk level, or whether the user is eligible to participate in a specific financial product. It is not meant to replace the openness of DeFi, but to provide an identity foundation for DeFi to expand into more real-world financial scenarios.

- Token Issuance, Airdrops, and DAO Governance

In token issuance, airdrops, and community incentive programs, a fully open wallet-address mechanism can easily lead to Sybil attacks, farming behavior, and difficulty enforcing jurisdictional restrictions.

On-chain KYC or identity credentials can be used to determine whether a user is a real and independent participant, comes from an allowed jurisdiction, meets campaign requirements, or holds a certain community contribution status. In DAO governance, it can also support one-person-one-vote mechanisms, verified contributor access, and reputation-based governance.

- Cross-chain Asset Access and Ecosystem Application Authorization

In a multi-chain environment, users may move across different public chains, wallets, DApps, payment applications, and RWA platforms. If every application builds a separate KYC process, the user experience becomes fragmented.

On-chain KYC allows users to hold reusable identity credentials and prove specific conditions across different applications on demand. For example, an application may verify user eligibility before allowing cross-chain asset access, unlock different functions based on identity conditions, or allow the user to authorize an application to read a specific verification result. This turns identity from a single platform’s account information into a reusable authorization capability across the Web3 ecosystem.

Is On-chain KYC a Guarantee? Where Are Its Boundaries?

On-chain KYC is not an absolute guarantee. It cannot guarantee that a user will always be trustworthy, nor can it guarantee that an asset, protocol, or transaction is completely safe. It also cannot replace legal documents, custody arrangements, risk control systems, audits, or regulatory processes.

What on-chain KYC can provide is a verifiable compliance signal. In other words, at a certain point in time, a user or address can prove that it meets specific identity conditions, such as having completed KYC, not being from a restricted jurisdiction, meeting an age requirement, being eligible to participate in a certain product, or having completed KYB as a corporate entity.

Therefore, the boundaries of on-chain KYC need to be clearly understood.

- First, on-chain KYC is not a security guarantee.

A user completing KYC does not mean that the user will never engage in fraud, default, money laundering, account misuse, or other high-risk behavior in the future. KYC only shows that the user met certain identity conditions at the time of verification. It cannot predict all future behavior.

- Second, on-chain KYC is not a credit endorsement.

An address passing KYC does not mean that the project it participates in is reliable, nor does it mean that the assets it holds are risk-free. Protocol security, asset quality, yield sources, custody arrangements, and market volatility still need to be evaluated separately.

- Third, on-chain KYC is not a regulatory exemption.

Even if an application uses on-chain KYC, it does not automatically meet regulatory requirements in all jurisdictions. Different countries and regions have different requirements for stablecoins, RWA, payments, lending, securities-like assets, and virtual asset services. On-chain KYC can help applications execute identity condition checks, but it cannot replace a complete legal and compliance assessment.

- Fourth, on-chain KYC does not mean making user identities public on-chain.

A properly designed on-chain KYC system should avoid putting raw personal information such as ID documents, passports, addresses, or facial data onto a public blockchain. It should use off-chain verification, encrypted credentials, selective disclosure, and zero-knowledge proofs, so that applications only verify necessary conditions rather than reading a complete identity profile.

More accurately, on-chain KYC is an identity verification and compliance decision-making tool. Its purpose is not to create “absolute trust,” but to provide a more verifiable, reusable, and privacy-friendly identity foundation in scenarios that require access control, eligibility checks, and risk tiering.

For Web3, the significance of on-chain KYC is not to turn all applications into permissioned systems. Instead, in real-world scenarios such as stablecoin payments, RWA, PayFi, lending, merchant services, and on-chain financial products, it helps applications answer a more specific question: does this user or entity meet the identity conditions required by the current scenario?

What Challenges Does On-chain KYC Face?

On-chain KYC is a valuable direction, but it also faces several challenges.

- Trust in Issuers

The entire system depends on trusted issuers. If an issuer is unreliable, the credibility of the credential itself is also affected.

Therefore, applications need to clearly define which issuers are accepted, how issuers conduct reviews, and how credentials are managed.

- Credential Revocation and Expiry

User eligibility may change, credentials may expire, jurisdictional rules may be updated, and some users may need to be removed from an access list.

Therefore, an on-chain KYC system must support credential expiry, revocation, and update mechanisms.

- Privacy Design Risks

If the system is poorly designed, privacy leakage may still occur even if raw identity data is not stored on-chain. Metadata, repeated proofs, address correlation, and other patterns may still expose sensitive information.

On-chain KYC needs to prioritize privacy design from the beginning.

- User Experience

If identity verification, credential storage, proof generation, and application authorization processes are too complex, users may easily drop off.

For on-chain KYC to gain wider adoption, it must work with better wallet experiences and lower-barrier login methods.

- Regulatory Differences Across Jurisdictions

KYC requirements vary across countries, regions, asset types, and business scenarios.

On-chain KYC infrastructure needs to be flexible enough to support different compliance rules, rather than serving only a single scenario.

- Interoperability

Web3 identity should not become a new silo.

Credential formats, DID systems, proof systems, verification rules, and application integration methods need to support interoperability across applications and ecosystems.

These challenges show that on-chain KYC cannot be just a simple identity verification plugin, nor can it rely only on a single platform’s centralized database. It needs to be designed as a more complete Web3 identity infrastructure: one that supports off-chain identity verification and credential issuance, user-held credentials, selective disclosure, on-chain verification, credential revocation, and cross-application reuse.

For real-world financial scenarios such as stablecoin payments, RWA issuance, PayFi, lending, and merchant services, the identity layer also needs to work together with the underlying public chain infrastructure. Only when identity verification, asset issuance, payment settlement, cross-chain liquidity, and compliance rules can coordinate within the same infrastructure can on-chain KYC truly move from concept to usability.

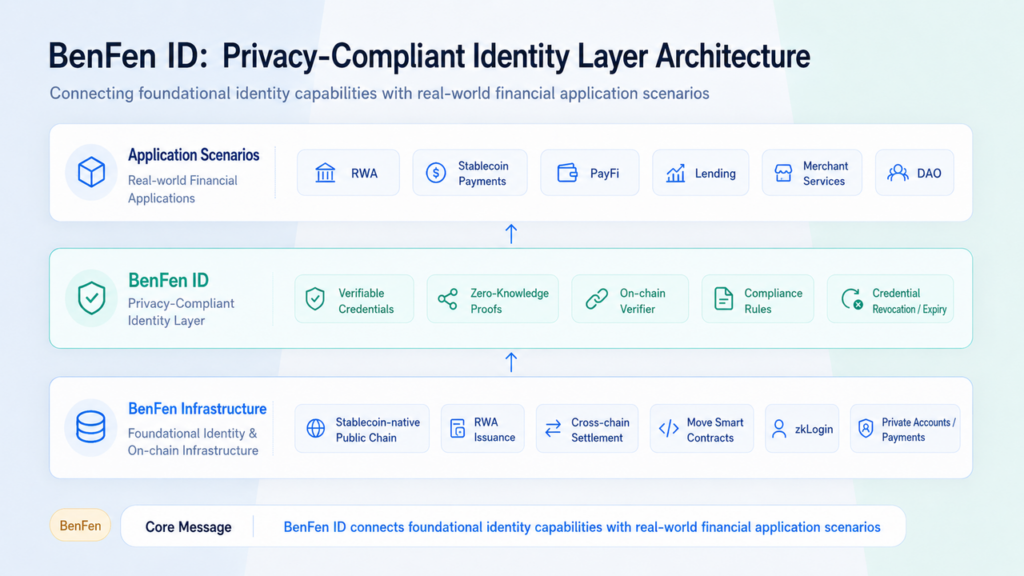

Against this backdrop, BenFen ID can be understood as a privacy-compliant identity layer within the BenFen ecosystem, built for stablecoin and RWA scenarios.

BenFen ID: A Privacy-Compliant Identity Layer for Stablecoins and RWA

As stablecoins, RWA, and payment applications become more deeply integrated with real-world financial activities, the importance of identity infrastructure is increasing.

BenFen Public Chain is building BenFen ID around this direction. It is a privacy-compliant identity layer within the BenFen ecosystem, designed to help applications complete necessary identity condition checks without exposing complete personal information.

The core idea of BenFen ID can be summarized as: verify once, self-hold credentials, prove on demand, and verify on-chain.

After completing identity verification, users can hold identity credentials issued by an issuer. When an application needs to verify a certain condition, the user generates a proof based on the local credential, and the on-chain verification contract checks whether the proof satisfies the required rules.

This model is especially suitable for scenarios such as PayFi applications, stablecoin payments, RWA issuance, merchant services, lending protocols, compliant financial products, DAO governance, and cross-chain asset access.

In the BenFen ecosystem, BenFen is positioned more as the underlying infrastructure layer, providing capabilities such as a stablecoin-native public chain, on-chain asset issuance, cross-chain settlement, compliance verification, and identity credentials. BenPay, by contrast, is closer to the application layer, serving PayFi, stablecoin payments, card spending, on-chain financial services, and real-world payment scenarios. Therefore, BenFen ID can be understood as an infrastructure layer that connects foundational identity capabilities with concrete application scenarios, allowing ecosystem applications such as BenPay to call verifiable identity results for payment access, merchant services, risk tiering, or eligibility checks for specific financial products.

For example, an RWA platform may need to verify whether a user has completed KYC and meets the access requirements of their jurisdiction. A stablecoin payment application may need to verify a user’s identity status before enabling higher limits. A lending protocol may need to confirm whether a user is eligible to use a specific product.

Through BenFen ID, these checks can be completed through reusable credentials and on-chain verification logic.

- Applications receive the verification results they need.

- Users reduce repeated KYC submission processes.

- Sensitive identity data does not need to be publicly exposed on-chain.

This allows Web3 financial applications to achieve a better balance between compliance, privacy, and user experience.

Why Is BenFen Suitable for Building On-chain KYC Infrastructure?

BenFen is not simply a general-purpose public chain. It is a stablecoin-native public chain built for stablecoin payments, RWA issuance, and on-chain financial applications.

This makes the identity layer especially important for the BenFen ecosystem.

- Stablecoin payments require trust and usability.

- RWA issuance requires compliant access control.

- Cross-chain settlement requires security.

- Financial applications require programmable rules.

- Users need privacy protection and a low-barrier experience.

BenFen’s infrastructure naturally aligns with the needs of on-chain KYC.

The Move smart contract environment provides a safer development foundation for asset and identity logic. The use of stablecoins as gas reduces the barrier for users to interact on-chain. zkLogin allows users to enter Web3 through more familiar login methods. Native cross-chain capabilities connect asset liquidity across multiple chains. Privacy-oriented account and payment designs also provide support for more sensitive financial scenarios.

On this foundation, BenFen ID further complements the identity verification layer.

It allows applications such as stablecoins, RWA, PayFi, lending, and merchant services to complete compliance verification through reusable identity credentials, rather than requiring each application to repeatedly collect user identity data.

From this perspective, BenFen ID is not an isolated feature. It is an important part of BenFen’s broader effort to build compliant on-chain financial infrastructure.

The Future of On-chain KYC and Web3 Compliance

The future of Web3 compliance should not be about copying centralized KYC databases onto the blockchain. A more reasonable direction is to build privacy-preserving identity infrastructure. Users should not have to repeatedly submit the same documents to every application. Applications should not collect more personal information than necessary. Regulators and institutions need clearer risk controls. Developers need programmable identity tools. On-chain financial products need compliant access mechanisms.

On-chain KYC connects these needs. It allows Web3 applications to verify identity conditions without exposing complete identities. It can support more compliant stablecoin payments. It can help RWA platforms manage investor eligibility and transfer restrictions. It can help payment applications adapt to real-world financial requirements. It also gives users stronger control over how their identity credentials are used.

As blockchain moves from speculative trading toward real-world financial applications, identity will become an important part of the infrastructure. BenFen’s exploration of on-chain KYC reflects this trend. By combining stablecoin-native infrastructure, RWA issuance capabilities, privacy-preserving verification mechanisms, and a low-barrier Web3 access experience, BenFen is building a more practical model for compliant on-chain finance.

On-chain KYC is not the opposite of decentralization. If designed properly, it can become a bridge between Web3 privacy and real-world compliance.

On-chain KYC FAQ

What is on-chain KYC?

On-chain KYC is an identity verification framework based on blockchain and cryptographic mechanisms. It allows applications to verify whether a user meets specific identity or compliance conditions. It does not mean storing raw personal identity data directly on-chain.

Will on-chain KYC expose my real identity?

A properly designed on-chain KYC system should not publicly expose a user’s real identity. It usually verifies specific conditions through signed credentials, selective disclosure, and zero-knowledge proofs, rather than displaying a complete identity profile.

What is zero-knowledge KYC?

Zero-knowledge KYC means that users can prove they meet a certain KYC or identity condition without revealing the underlying personal data to the application. For example, a user can prove that they have completed KYC without exposing their ID number or address.

Why does RWA need on-chain KYC?

RWA products often involve investor eligibility, jurisdictional restrictions, transfer rules, and compliant access. On-chain KYC can help make these rules programmable and verifiable at the smart contract level.

Why do stablecoin payments need on-chain KYC?

Stablecoin payment and settlement applications may need user tiering, merchant verification, jurisdictional access rules, and limit management. On-chain KYC can support these compliance needs while reducing repeated data collection.

What is BenFen ID?

BenFen ID is a privacy-compliant identity layer within the BenFen ecosystem. It supports identity verification, user-held credentials, proof generation on demand, and on-chain verification logic that allows applications to determine whether a user meets specific identity conditions.

Does on-chain KYC mean uploading my ID card to the blockchain?

No. A well-designed on-chain KYC system should keep raw identity materials off-chain and only verify credentials, proofs, or verification results on-chain.

Can on-chain KYC balance privacy and compliance?

Yes. The goal of on-chain KYC is to allow applications to verify necessary compliance conditions while minimizing the exposure of users’ personal information.

Is on-chain KYC a guarantee?

No. On-chain KYC cannot guarantee that a user will always be trustworthy, nor can it guarantee that an asset, protocol, or transaction is completely safe. What it can provide is a verifiable compliance signal: at a certain point in time, a user or address can prove that it meets specific identity conditions, such as having completed KYC, meeting jurisdictional access requirements, or being eligible to participate in a certain product. Therefore, on-chain KYC should be understood as an identity verification and compliance decision-making tool, not an absolute credit endorsement.